Achmea: Niche becomes a building block - SRTs within alternative credit

This article was originally written in Dutch. This is an English translation

Significant Risk Transfer (SRT) transactions are gaining ground among pension funds and insurers. They offer exposure to credit risk on well-diversified core banking portfolios, often with variable spread income, and usually without the underlying loans being removed from the bank’s balance sheet.

By Serdar Özdemir, Capital Markets Manager, Achmea

In this article, we discuss how SRTs work, their position within alternative credit, and the questions an investment committee will want to have clarified in advance.

What is an SRT and why do banks use them?

Banks maintain provisions for expected losses and capital for unexpected losses. Basel 3.1 may limit the benefits of internal models, which could increase the capital requirements for certain portfolios. This encourages banks to manage credit risk more actively.

An SRT transaction is a transaction in which a bank economically transfers a defined portion of the credit risk to third parties in order to improve capital efficiency. This does not automatically result in capital release. Regulators assess, among other things, the transaction structure, the quality of credit protection and the prudential recognition of the risk transfer.

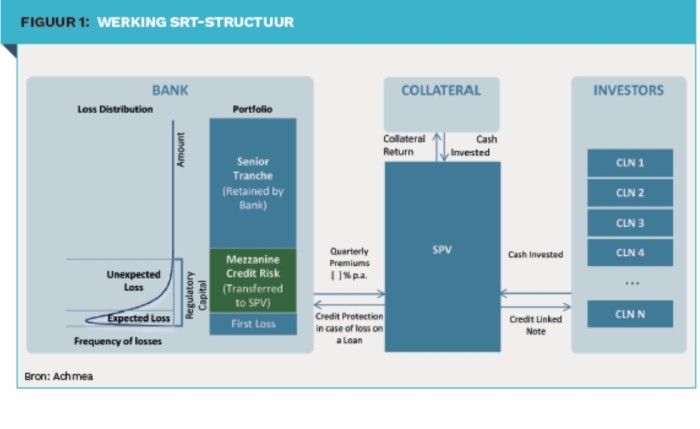

How does the structure work in practice?

Many SRTs are synthetic securitisations. The bank tranches the credit risk of a reference portfolio (e.g. SME, consumer or mortgage loans) and purchases credit protection on a specific tranche. Legally, loans generally remain on the bank’s balance sheet, whilst economically a portion of the risk is shifted. For investors, the risk-return profile lies mainly in junior and mezzanine positions: the premium is higher because these tranches absorb losses first as soon as losses breach the buffer (attachment). This makes the investment an exchange: a premium in exchange for a defined credit risk.

- Funded: the protection is financed, often via Credit-Linked Notes (CLNs) issued by an SPV, with the proceeds held as collateral.

- Unfunded: the protection is provided via a guarantee or insurance, making counterparty and documentation risks more significant.

- Cash flow: the bank pays a premium; investors receive the coupon from this premium, supplemented (in the case of funded structures) by the return on the collateral. Losses are absorbed via the tranche waterfall.

SRTs typically offer access to large, bank-originated reference portfolios with broad diversification and a more standardised credit process.

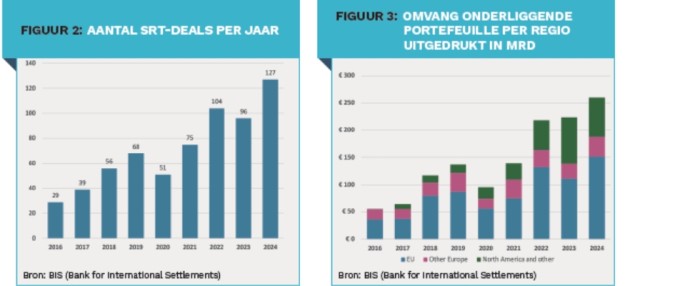

Market development: from niche to a more mature segment

The market for synthetic SRTs has grown significantly in recent years.1 In the IACPM Global SRT Bank Survey (2016–2024), 51 banks reported more than 650 transactions, with a total of approximately €1.3 trillion in underlying loans. Europe is dominant: approximately 70% of activity in 2024 came from EU banks.

Dutch institutional investors are also visibly active. PGGM has publicly stated that it has been investing in SRTs since 2006 and, as at 31 December 2024, reported 42 transactions with a market value of €6.7 billion and a historical average realised return of around 12% per annum (up to and including 2024). 2 Past performance is no guarantee of future results and varies by tranche, portfolio and market conditions.

Positioning within alternative credit

SRTs are often compared with CLOs, private ABS and direct lending. The differences lie primarily in the nature of the underlying assets and in how risk is reflected in the valuation. It is precisely here that the core of the allocation case often lies for institutional investors. Whereas direct lending and CLOs more often provide exposure to relatively more concentrated portfolios and/or manager-driven credit selection, SRTs typically offer access to large, bank-originated reference portfolios with broad diversification and a more standardised credit process. This does not mean that the risk is necessarily lower, but rather that it is of a different nature: the outcome depends more on portfolio construction, tranche positioning (attachment/detachment) and the contractual definitions surrounding credit events and recoveries (for example, when a ‘default’ is counted and how losses/recoveries are determined and allocated), than on individual borrower selection. For an investment committee, this makes SRTs within alternative credit more comparable in terms of portfolio logic (data, loss mechanics, governance) than by label, which aids allocation, monitoring and communication to the board.

- Underlying assets: SRTs often refer to core bank loans, whilst CLOs typically refer to leveraged loans. Direct lending is bilateral and less standardised; private ABS is heterogeneous and often asset-specific.

- Valuation and liquidity: SRTs are often private instruments. As a result, measured (MTM) volatility may appear lower, but this also depends on the valuation frequency and pricing governance.

- Diversification: SRTs can offer diversification relative to public credit and competitive direct lending, but the extent of this depends on the tranche and portfolio and requires stress testing against default and recovery scenarios.

|

5 themes on which an investment committee usually asks questions: Portfolio: composition (sector/geo), underwriting standards, concentration limits, duration (WAL) and transparency (reporting). Investment case: tranche attachment/detachment, expected loss (base and stress), definitions of credit events and recovery methodology, expected return relative to the risk incurred. Structure: funded/unfunded, collateral quality and custody, waterfall, replenishment/managed features and legal enforceability. Governance & Regulation: valuation policy (model/quotes), liquidity assumptions, monitoring and escalation to risk/IC. Regulation: WTP and Solvency II treatment and sensitivity to changing rules or interpretations. |

Wtp and Solvency II: relevant, but dependent on the details

For Dutch pension funds, the increased interest coincides with the transition to Wtp. SRTs may be suitable as a complement within alternative credit, provided that liquidity policy, valuation governance and risk budget align with the chosen tranches.

For Dutch pension funds, the appeal of SRTs lies in an additional source of variable spread income and diversification towards core banking portfolios.

For insurers, the capital treatment under Solvency II is often decisive. Historically, capital requirements for securitisations were relatively high. From 30 January 2027, the revised Solvency II regulations provide for more favourable treatment of securitisations, particularly for senior tranches and STS positions, and to a lesser extent for mezzanine and junior tranches. Insurers with a (partial) internal model can, depending on model approval and assumptions, model diversification and loss distribution more explicitly, which may reduce the capital burden. SRTs are an interesting alternative, particularly for parties that can invest in junior tranches of CLOs using an available risk budget or a favourable internal model. The underlying rationale is that bank-originated portfolios are generally established under stricter underwriting and governance and are often more granularly diversified, whereas CLO portfolios are built up through manager selection and market opportunities, meaning that risk dynamics and concentration may, by definition, differ.

What does this mean for Dutch pension funds?

SRTs have evolved from a niche instrument into a more mature segment within alternative credit. For Dutch pension funds, the appeal lies in an additional source of variable spread income and diversification towards core banking portfolios, with the ability to steer the risk-return profile through tranche selection (and attachment/detachment) within the WTP risk budget.

For funds with sound governance, SRTs offer one of the more attractive risk-return combinations within the current alternative credit universe.

|

SUMMARY SRTs are growing rapidly within the alternative credit segment and offer access to credit risk on well-diversified core banking portfolios. The market is maturing. Globally, there are more than 650 transactions by 51 banks and €1.3 trillion in underlying loans. Europe is leading the way. Dutch investors such as PGGM have been active for years. For pension funds, SRTs can fit within the risk budget as an alternative with variable spreads. Insurers, particularly those using (partial) internal models, can – depending on model approval and tranche selection – use them to reduce their capital burden. |

- IMF Working Paper: ‘Recycling Risk: Synthetic Risk Transfers’

- PGGM: CRS at PGGM – public information on SRT/CRS activities (reference date 31 December 2024).

Read the full article in Financial Investigator magazine