Harry Geels: Inflation isn’t just about the money supply

")

This column was originally written in Dutch. This is an English translation.

By Harry Geels

Milton Friedman often said: ‘Inflation is always and everywhere a monetary phenomenon’, a statement that is often misquoted as ‘inflation is a policy’. It is a powerful statement with a grain of truth, but the story of inflation is broader than that.

The statement originates from a famous lecture given by Friedman in Bombay in 1963, entitled ‘Inflation: Causes and Consequences’. In it, he defined inflation as a ‘steady and sustained rise in prices’ and stated that it can only arise if the money supply grows faster than ‘output’, or the production of the real economy.

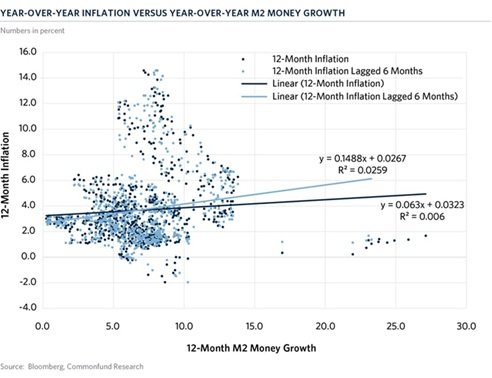

Later, this was supplemented by well-known sayings such as ‘inflation is a policy’ and ‘inflation is hidden taxation’. These are powerful ‘one-liners’ that certainly explain part of the price rises. Yet they do not tell the whole story of inflation. The figure below, for example, shows the relationship between the 12-month change in the money supply (M2) and 12-month inflation. There is only limited statistical significance between the two: a larger money supply leads to inflation only to a limited extent.

Where Friedman is right

Let us start with what remains valid of Friedman’s statements. In the long run, it is difficult to separate inflation from monetary policy. If the money supply grows structurally faster than the real economy, this must translate somewhere into higher prices. With his statements, Friedman has in fact given wings to Irving Fisher’s well-known (rewritten) equation (MV=PY). If the money supply (M) increases and the velocity of money (V) and output (Y) remain constant, P rises.

Central banks ultimately determine (via the banks) the nominal anchor. Without monetary space, inflation dies out. If, for example, oil prices rise due to a war and central banks do not increase the money supply, then after an initial inflationary shock prices will fall rapidly because either output or the velocity of money must decrease. A well-known saying goes: ‘The best remedy for high oil prices is high oil prices’, at least if central banks do not intervene.

But inflation is not just about the money supply

Anyone who tries to understand inflation purely in terms of the money supply will get stuck. In the shorter term, inflation consists of three components. The first concerns the Fisher equation. Inflation is then equal to the sum of the change in M and the change in V minus the growth in output. In addition, we have the supply shocks discussed earlier, such as the rise in energy prices due to a war and problems in supply chains, as was the case during the coronavirus pandemic.

The other component is what I call the price transmission mechanism: the extent to which inflation can actually feed through to the economy. This depends largely on three factors. Firstly, consumer expectations. Inflation (or deflation) can play on consumers’ minds. Expectations of higher inflation are reinforced by increased spending, and vice versa: in the event of deflation, we tend to postpone spending, thereby reinforcing the downward spiral.

Secondly, there is the market power of companies. If this increases – as with the emergence of monopolies and oligopolies – they can more easily implement price rises (where there is more competition, price rises are dampened). Thirdly, institutions play a role. Consider governments that engage in price regulation, or even contribute to inflation themselves, for example through higher local taxes and excise duties. Another institutional example concerns (mandatory) indexation of wages, rents and pensions.

Inflation is more of a redistribution process

In my model, inflation is not a neutral figure, but a redistribution process. When energy prices rise, households lose out. The resources do not disappear; they shift: to energy producers, or more generally, to sectors with pricing power. With excise duties, the government gains and the consumer loses. Inflation is therefore not an abstract macro-phenomenon, but a concrete shift in purchasing power – Friedman’s ‘hidden tax’, so to speak, but in a more nuanced form.

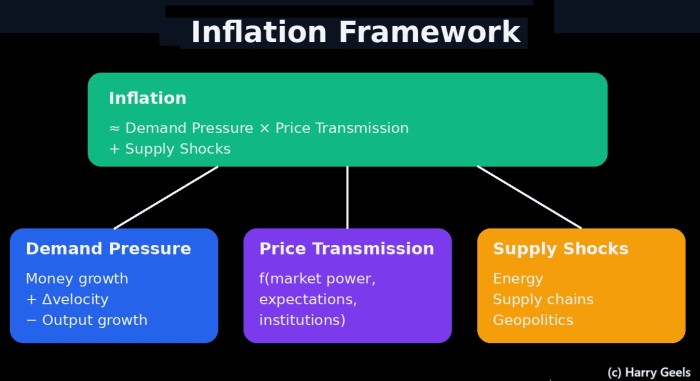

The question is therefore not just how much money is in the system, but how that money moves through the economy and how prices react to it. No longer just the M, but a distinction between demand, transmission and shocks. In a formula: Inflation ≈ Demand Pressure × Price Transmission + Supply Shocks. Inflation therefore has three layers: where it starts (often in real shocks), how it works through (via market power, wages and expectations) and how long it lasts (where monetary policy is ultimately decisive).

In conclusion

All this also explains why recent inflation is so difficult to interpret. During the GFC, the money supply grew strongly, but inflation failed to materialise. V fell and there was widespread pessimism. During the pandemic, the opposite happened. Demand recovered quickly, supply lagged behind, and increasingly powerful companies had scope to raise prices. Perhaps the best way to rephrase Friedman’s proposition is: ‘The money supply determines how long inflation lasts. The economy determines where it starts and who pays for it.’

This article contains a personal opinion by Harry Geels